{kind=link}

The $12M Ceiling: Why Top Loan Officers Are Leaving Legacy Retail for Canopy’s Proprietary Stack

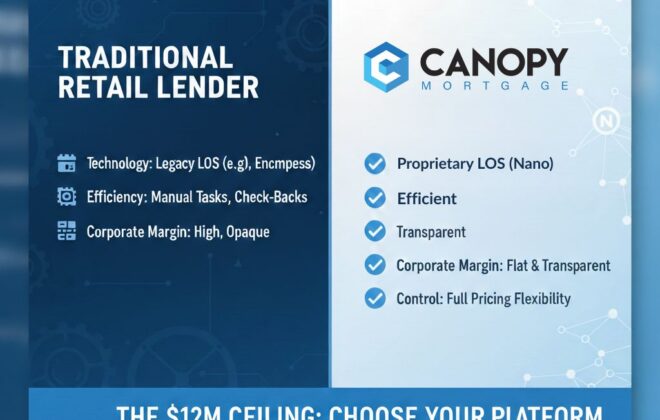

{{ brizy_dc_global_blocks position=’top’ }}The $12M Ceiling: Why High-Volume Loan Officers are Switching to Canopy MortgageFor loan officers producing $12M+ annually, traditional retail lending structures often become a bottleneck. It’s not just about compensation—it’s about the drag of legacy mortgage technology and bloated corporate layers. At…

{kind=link}

Escaping Corporate Bloat: How Canopy Mortgage’s Nano Tech Scales Your Business

{{ brizy_dc_global_blocks position=’top’ }}Escaping Corporate Bloat: Scale Your Production with the Canopy Mortgage P&L ModelIn 2026, the traditional retail mortgage model is failing high-producers. Feeding a massive corporate hierarchy with your hard-earned commission no longer makes sense. This is why a new wave of top-tier…

{kind=link}

Nano vs. The Rest: Why a Unified Codebase Matters for Loan Officers

{{ brizy_dc_global_blocks position=’top’ }}Nano vs. Legacy LOS: Why a Unified Codebase is the Ultimate Competitive AdvantageHow much of your day is spent staring at a spinning wheel on your screen? If you are a Loan Officer working with legacy systems like Encompass, the answer is…

{kind=link}

Is Canopy Mortgage a broker?

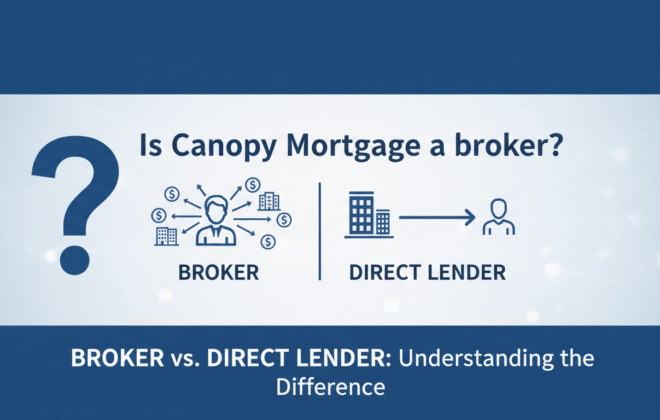

Is Canopy Mortgage a broker? The Short Answer: No. Canopy Mortgage is a Direct Lender (Mortgage Banker). Let’s address the elephant in the room. A lot of Loan Officers look at our pricing model, our flat fees, and our autonomy, and they ask: “Wait, is…